Why Should I Lease My Next Vehicle?

Why Should I Lease My Next Vehicle?

Less cash down...

Don't put too much cash down. Keep your money in the bank. Consider if you were to have an accident a couple months after you start your lease. The portion of the vehicle that you owe on the vehicle is probably more than what your insurance will cover. But, with a lease through Handy Buick GMC Cadillac, GAP insurance is included with your lease. GAP insurance takes care of the difference in what you owe and what the vehicle is worth. If you put money down on the lease, that difference between what the insurance pays and what the bank needs to pay off the lease is going to be paid with the cash you put down. Keep your money so you can use it and let the GAP insurance cover you. Ideally with a lease, you make your first payment and drive it home.

Banks are more strict about who qualifies for a lease...

The bank is taking more risk. The bank is not charging you for a major portion of the vehicle (the residual). They are taking the chance the vehicle will be worth what they think it will be worth in a couple years. In addition, while you are making payments on the lease, the bank is also receiving less money from you every month (leases generally have lower monthly payments). If you were to stop making payments on a lease, the bank would have less money because they got less money from you per month. Because the bank is taking this higher risk, they generally only will accept a lease contract with someone with a proven record or paying off their obligations. If you can get a bank to take more risk than yourself you can be sure you are getting better financial situation.

You stay under factory warranty for the entire lease…

If you have a 3 year/12,000 mile a year lease you will be covered with a bumper to bumper warranty for the length of the lease term. Rest assured, you will not need to pay more to keep your vehicle running while you are still making payments on it. Even if you plan to drive more miles than what would be covered under a standard manufacturer warranty during your lease term, we can extend your warranty for the extra mileage and add it to your lease payment.

You get a car with the newest safety features every couple years...

We often hear people say they "don't need all the bells and whistles" they get with a new car. Luxury features are great but more importantly consider the safety features you can get with a newer vehicle. Rear view camera, automatic braking systems, lane change alert, dynamic cruise control are all features that were not as common a couple years ago. Buying a newer vehicle ensures you have an opportunity to get the latest safety on your vehicle sooner. More and more safety is becoming standard with each new model year. Leasing is an easier way to get those features as soon as possible.

You can prepare for life changes better when you lease...

Some times you get a new vehicle and you realize it is not going to fit your life. You have a new baby, you get a dog, or you move somewhere that you need a 4 wheel drive. Whatever happens you know that at the end of the short lease term, no matter what the vehicle is worth, you can walk away from it to get yourself in a new vehicle that meets your needs.

Some people say they don't want to lease because they never own the vehicle.

If you have a 6 or 7 year loan, you do not own the vehicle until that last payment. At the end of that time, you then own a 7 year old vehicle with around 84,000 miles. If you had been leasing during that 6-7 years, you could have had two vehicles and even been a year into a third vehicle each with with the newest features, less chance of needing repairs in the first place and been under warranty the entire time. None of your friends would ever tell you something like "Good thing you bought that car. Now that you paid it off, it is out of warranty and it has 84,000 miles. Way to go!" On the other hand, your friend might say, "Is this a new car? Didn't you just get your last car like 2 and a half years ago? This one is even nicer too. You must be doing well."

What if I drive a lot of miles?

Knowing how many miles you will drive during your lease term is going to save you frustration in the future. That is true. It often than not does not matter how many miles you drive, leasing is going to be a more sound financial decision. Figure out how many miles you have have driven the last couple of years. Set up your lease to cover the miles you most likely will be driving during the term. Most leases are for 12,000 miles per year. You can save on your monthly payment by doing a 10,000 mile a year lease. Sometimes you can even set up an 8,000 miles per year lease if that is what you drive. Watch out for advertised monthly lease payments that sound too good to be true. If you hear, "Super low mileage lease" it probably means they are including 8,000 miles per year. If you build a 8,000 miles/year lease, at the end of the lease the bank will be expecting the vehicle to be in 8,000 miles/year condition. If you drove the vehicle more than the contract was written for, the bank expect then they will be looking for you to make up the difference. It is much cheaper to build in those miles up front. If you drive more like 15,000 or 20,000 miles a year it is a good idea to set the lease up appropriately at the very beginning. Think of a lease as paying for the portion of the car you are going to use. Kind of like a stick of butter. If you think you will only use half a stick of butter to make a cake, why buy the entire stick of butter. Just pay for the half you know you will use. You can cut up a stick of butter into whatever size you need. If you are going to only use 50% (12,000 miles/year), pay for 50%. If you are going to only use 30% (8,000 miles/year), only pay for 30%. If you are going to use 75% (20,000 miles/year) then pay for only 75%. The lease contract lets you slice the car into the portion that you think you will use and then let the bank worry about the residual portion after you are done using it.

Customize your ride...

If you like to customize your vehicle by drilling into the body or adding powertrain upgrades, regardless of how much those parts are worth, the bank does not want those on the vehicle when you turn it in. They are considered negative when they go to resell it. All the used vehicle guides on stock vehicles that are equipped as when they left the factory. If you want to add aftermarket parts to your vehicle then you probably should not lease. There is good news though. Most of the popular features that can previously were only available as aftermarket parts can now be factory installed. For example, if you want a remote engine starter or upgraded suspension, we can add those parts as a factory or dealer installed feature. That way it is built into the lease at the very beginning and will not negatively affect the value of the vehicle at the end of your lease.

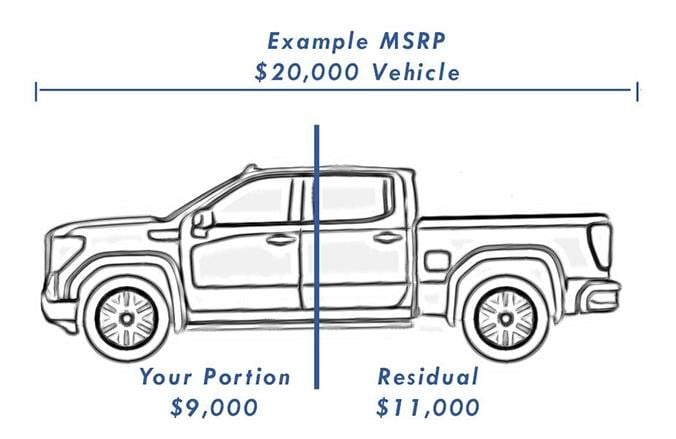

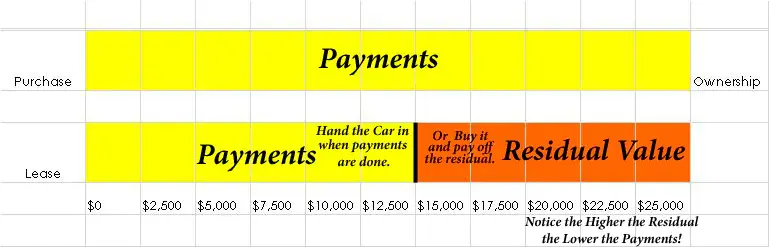

Unfortunately Vehicles Depreciate

Unfortunately vehicles depreciate, regardless of the one you buy. Yes, there are rare occasions, such as classic and exotic cars when a vehicle increases in value. Generally speaking though, a vehicle you use as a daily driver is going to depreciate. Check out the graph to compare leasing versus purchasing with a traditional loan. Just like a stick of butter, you can use it a little at a time. Butter doesn't cost thousands of dollars though. A lease enables you to only pay for the amount of the vehicle you are going to use.

The amount you are going to use is based on what the bank estimates the vehicle will be worth when you are done driving it in a couple of years. They take the current value, then they subtract the estimated future value (residual value) and then base your payments on the difference, or the depreciation. That is why you need to determine how many miles you think you are going to drive. If you drive 10,000 miles a year the value will be different than if you drive 18,000 miles per year. Once you are done with the vehicle, you hand it in, regardless of the actual value. It might be worth a lot less than they estimated. If you drove within the number of miles you said you would, you are all set. The bank is then responsible for selling the vehicle on the open market.

If for some reason the vehicle is worth more than they estimated, it might even be a good idea to purchase the vehicle that you leased. If you purchase the vehicle with a $10,000 residual but it is actually worth $12,000 you have an instant $2,000 equity. This is rare but it does happen. You can, in effect, purchase your own used vehicle.

Whether you hand the vehicle in or purchase it at the end, you know that you have the option. Your vehicle needs may have changed in three years. Maybe you realize you do not like the vehicle as much as you thought you would. Maybe you want the newest technology and the most up to date safety features. Leasing gives you a shorter purchasing cycle, allow you to more frequently update what you drive to meet your wants and needs. Purchasing a vehicle with a traditional loan leaves your options up to the used car market. If the market is soft you might not be able to trade in and get a new vehicle when you want to. Leasing puts you in more control of your decision.